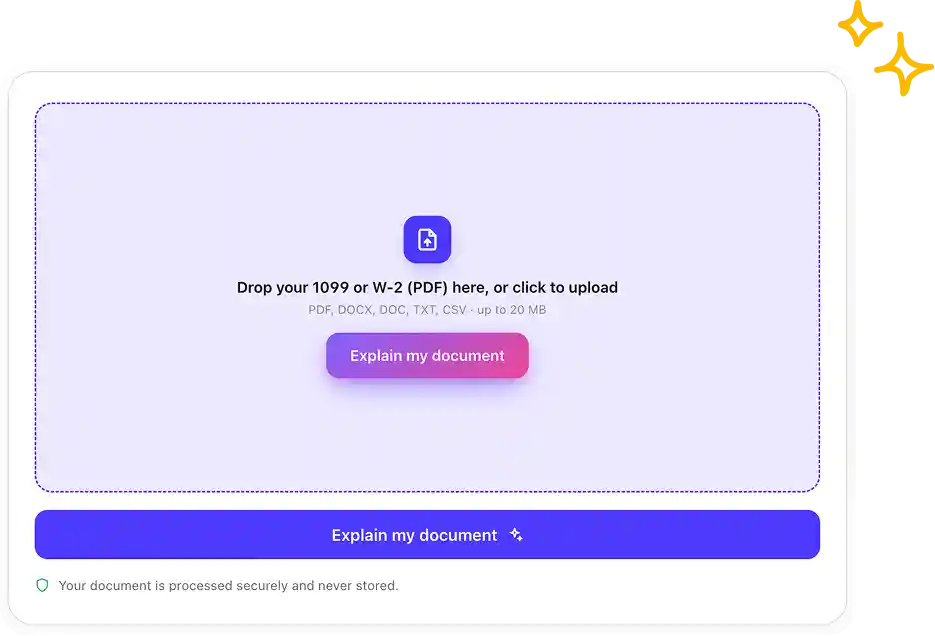

Paste your offer or upload a 1099 / W-2 form — the AI 1099 vs W-2 Explainer breaks down self-employment tax, withholding, deductions, benefits and worker classification side by side, then calculates which one nets you more after taxes. Built for freelancers, gig workers, contractors and anyone weighing a new role.

Understand long papers without reading them in their entirety — our AI assistant extracts the most important ideas, allowing you to grasp scientific research documents in seconds instead of hours.

Type your hourly rate, annual salary or contractor rate — or drop in a 1099-NEC, 1099-MISC or W-2 PDF. The AI 1099 vs W-2 Explainer picks up gross pay, withholding, state, and pay frequency automatically so you don’t hand-key anything.

The AI 1099 vs W-2 Explainer calculates self-employment tax (15.3% vs 7.65%), federal and state withholding, quarterly estimated payments, deductible business expenses, and the missing benefits (health, 401(k), PTO). The output is a side-by-side comparison with a clear net-income delta.

Read the breakdown, then ask anything in chat — “how much should I charge as a 1099 to match my W-2 take-home?”, “what’s the IRS test for worker classification?”, “when are quarterly taxes due?” Every answer cites the IRS rule or worksheet it came from.

USE CASES

Got a $90/hr contract 1099 offer and an $140k W-2 offer? The AI 1099 vs W-2 Explainer normalizes both to annual take-home after self-employment tax, FICA, federal and state withholding, plus the cash value of the W-2 benefits stack (health, 401(k) match, PTO). Side-by-side delta so you know which one actually pays more.

Going independent? On $100k of income, a 1099 contractor pays roughly $7,000 more in employment taxes than a W-2 employee. The AI 1099 vs W-2 Explainer calculates the exact 1099 hourly rate you need to clear the same take-home pay you had on W-2, factoring in self-employment tax, lost benefits and the QBI deduction.

If you expect to owe $1,000 or more, the IRS requires 1099 contractors to pay quarterly estimated taxes — April 15, June 15, September 15, January 15. The AI 1099 vs W-2 Explainer estimates each quarterly payment from your year-to-date income, projects the safe-harbor amount, and warns you about underpayment penalties before they hit.

Hiring a 1099 contractor when the IRS thinks they should be W-2 means back taxes, penalties and potential lawsuits. The AI 1099 vs W-2 Explainer walks you through the IRS common-law test — behavioral control, financial control, type of relationship — and flags arrangements that look more like employment, so employers and freelancers stay on the right side of the rules.

Home office, mileage, equipment, software, half of self-employment tax, health insurance premiums, retirement contributions — 1099 contractors can deduct business expenses W-2 employees cannot. The AI 1099 vs W-2 Explainer lists every deduction that applies to your situation and quantifies how much it shaves off your tax bill.

After the side-by-side, keep asking. “Can I be 1099 and W-2 at the same employer?” “What’s the QBI deduction worth on $150k of 1099 income?” “When are 1099 forms due?” The AI 1099 vs W-2 Explainer answers in plain English with citations back to IRS publications and the worksheets it used.

Enter your rate or upload the form — the AI 1099 vs W-2 Explainer shows the tax difference and net take-home in under a minute. Free to try, no signup.

Overchat AI brings you the power of the world's top AI models: ChatGPT, Claude, Gemini, Mistral, and more.

A W-2 is the tax form your employer issues if you're a regular employee — the company withholds federal income tax, Social Security, Medicare and state tax from your paycheck and pays the employer half of FICA. A 1099 (1099-NEC or 1099-MISC) is issued to independent contractors and freelancers — nothing is withheld, and you owe the full 15.3% self-employment tax plus federal and state income tax. The Overchat AI 1099 vs W-2 Explainer breaks down both side by side so you can see the real take-home difference.

Pure dollars: most workers net more on W-2 because the employer pays half of FICA, withholds taxes automatically and bundles health insurance, 401(k) match and PTO. 1099 makes sense when you can charge enough above your W-2 rate to cover the extra 7.65% self-employment tax and the lost benefits stack, and you want the business-expense deductions and schedule flexibility independent contractors get. The AI 1099 vs W-2 Explainer calculates the exact 1099 rate that matches your current W-2 take-home so the decision is numbers, not vibes.

1099 contractors owe the full self-employment tax of 15.3% — the employee 7.65% AND the employer 7.65% — because there's no employer paying the other half. W-2 employees only pay 7.65% out of pocket. On $100,000 of income that works out to roughly $7,065 more in employment taxes for a 1099 worker. The IRS does let you deduct the employer-equivalent half of SE tax from your adjusted gross income, which softens the hit, and the AI 1099 vs W-2 Explainer factors that in automatically.

Rule of thumb: take your W-2 hourly rate and multiply by about 1.25 to 1.40. That covers the extra 7.65% self-employment tax, the missing 401(k) match (typically 3–6%), employer-paid health insurance (often $500–$1,500/month), and PTO and sick days you no longer get paid for. So a $50/hr W-2 employee usually needs to charge around $63–$70/hr as a 1099 contractor to net the same after taxes. The AI 1099 vs W-2 Explainer runs this calculation against your real numbers — state, salary, benefits package — and gives you a precise breakeven rate.

Yes — if you expect to owe $1,000 or more in tax for the year, the IRS requires quarterly estimated payments on April 15, June 15, September 15 and January 15. Skip them and you owe an underpayment penalty even if you pay everything by April. W-2 employees don't have this problem because withholding covers it automatically. The AI 1099 vs W-2 Explainer projects each quarter's payment from your year-to-date income and shows you the safe-harbor number (the smaller of 100% of last year's tax, or 90% of this year's) so you're protected from penalties.

1099 contractors deduct business expenses directly against self-employment income on Schedule C: home office, mileage and vehicle expenses, equipment, software subscriptions, professional development, health insurance premiums (above the line), retirement contributions (SEP-IRA, Solo 401(k)) up to $69,000 in 2024, and half of self-employment tax. They also qualify for the 20% Qualified Business Income (QBI) deduction. W-2 employees lost almost all unreimbursed-employee-expense deductions in 2017. The AI 1099 vs W-2 Explainer lists every deduction that applies to your situation and quantifies the tax savings.

Not for the same role. The IRS doesn't let an employer classify the same job as both, because the underlying test is the nature of the working relationship, not what each side chose to call it. You CAN be W-2 at your day job and 1099 from a side client — millions of people are. You can also be W-2 from Employer A and a true independent contractor providing a distinct service to Employer A on a 1099 basis, but the IRS scrutinizes that arrangement closely. The AI 1099 vs W-2 Explainer walks through the IRS common-law test so you and your employer don't get hit with back taxes and penalties for misclassification.

Steep. Employers can owe the unwithheld federal income tax (1.5% of wages), the employee's unpaid share of FICA (20% of the employee portion), the full employer FICA match, a $50 penalty per missing W-2, and a 0.5% per month failure-to-pay penalty, plus interest. If the IRS finds the misclassification was intentional, the penalty jumps to 100% of the unwithheld tax. The Department of Labor can also tack on minimum wage and overtime back-pay claims, and affected workers can sue for unpaid benefits. The AI 1099 vs W-2 Explainer walks employers and workers through the IRS common-law test so the classification holds up.

Chinese company Baidu has quietly released a model that's just as good as DeepSeek and ChatGPT — ERNIE 4.5 delivers exceptional performance at a fraction of the cost — and most people outside China have never even heard of it.

If you're wondering: what is DeepSeek AI, the answer is quite simple. DeepSeek AI is a Chinese AI research lab that builds large language models. The company released several models in late 2024 and early 2025 that compete directly with OpenAI's GPT-4 and Anthropic's Claude, but at a fraction of the operating cost.

ChatGPT Plus costs $20 per month plus tax, while the Pro plan costs $200 per month plus tax. Understandably, not everyone is willing to pay that much for a chatbot, especially if the premium features aren’t worth it to them. This raises an obvious question: how can I use ChatGPT for free?

Available on Web, iOS, and Android. Access your AI assistant anywhere, anytime.